Understanding the Ist of Future Care Premiums May 2025: A Comprehensive Guide

Navigating the complexities of future care planning can be daunting, especially when financial considerations like premiums come into play. The phrase “ist of future care premiums may 2025” likely refers to a specific schedule, rate sheet, or projection related to the costs associated with long-term care insurance policies or other future care arrangements effective or reviewed in May 2025. This guide aims to provide a deep understanding of what this might entail, offering clarity and actionable insights to help you make informed decisions about your future care needs. We’ll explore the factors influencing these premiums, analyze potential scenarios, and provide expert guidance on securing the best possible coverage.

What Exactly is “Ist of Future Care Premiums May 2025”?

This phrase most likely refers to a detailed listing, schedule, or projection of premiums associated with future care policies, specifically as they are understood or projected in May 2025. To truly understand this, we need to break down the key components:

* **Future Care:** This broadly encompasses various services and arrangements designed to provide care and support to individuals in their later years or when they require assistance due to age, illness, or disability. This can include long-term care insurance, assisted living facilities, in-home care, and other related services.

* **Premiums:** These are the periodic payments (typically monthly or annually) required to maintain an active insurance policy or care agreement. The premium amount is determined by various factors, including the type of coverage, the age and health of the insured, and the benefit levels selected.

* **May 2025:** This specifies a particular point in time. The significance of May 2025 could be that it represents the date when new premium rates are scheduled to take effect, or when existing policies are reviewed and adjusted.

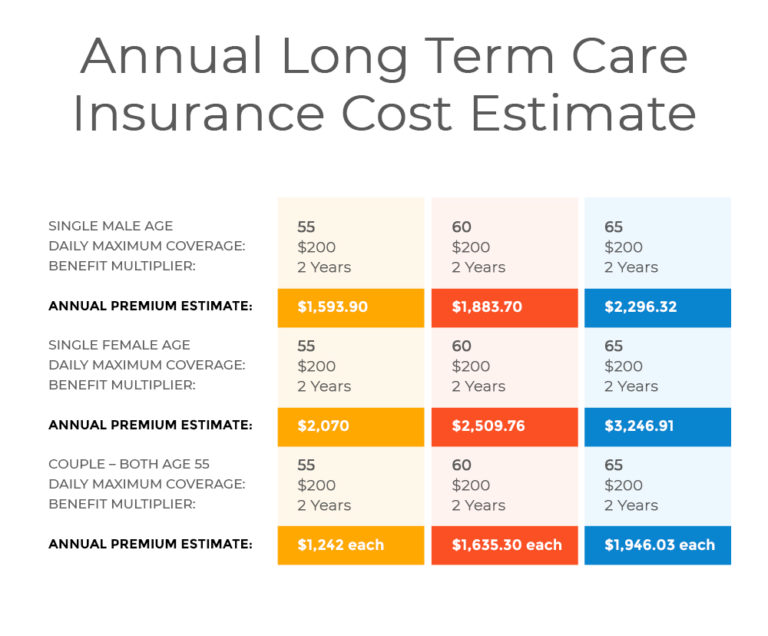

Essentially, “ist of future care premiums may 2025” probably refers to a document or dataset outlining the anticipated or actual costs of future care policies as they stand in May 2025. This information is crucial for individuals planning for their long-term care needs, as it provides insights into the potential financial burden and helps them make informed decisions about coverage options. Recent trends indicate that long term care costs are on the rise, and understanding the premiums associated with future care is becoming increasingly important.

Factors Influencing Future Care Premiums

Several factors can influence the premiums associated with future care policies. These include:

* **Age:** Generally, the older you are when you purchase a policy, the higher the premiums will be. This is because older individuals are statistically more likely to require care sooner.

* **Health:** Your current health status plays a significant role in determining premiums. Individuals with pre-existing health conditions may face higher premiums or even be denied coverage.

* **Coverage Level:** The extent of coverage you choose directly impacts premiums. Policies with higher benefit levels, longer coverage periods, or more comprehensive services will typically have higher premiums.

* **Inflation:** Future care costs are subject to inflation, which can significantly impact premiums over time. Policies with inflation protection riders will generally have higher initial premiums but can help mitigate the impact of rising costs in the future.

* **Interest Rates:** Interest rates play a crucial role for insurance companies in pricing their products. Higher interest rates mean that insurance companies can invest the premiums they collect and earn more money, which can lead to lower premiums for consumers. Conversely, lower interest rates can lead to higher premiums.

* **Mortality Rates:** Mortality rates are another important factor that insurance companies consider. If people are living longer, they are more likely to need long-term care, which can lead to higher premiums.

* **Policy Features:** The specific features and riders included in a policy can also affect premiums. For example, a policy with a shorter elimination period (the time you must wait before benefits begin) will typically have higher premiums than a policy with a longer elimination period.

Understanding the Implications of May 2025

May 2025 could be a significant date for several reasons. It might mark the beginning of a new rate cycle for insurance companies, reflecting updated actuarial data and economic forecasts. It could also be the date when existing policies are reviewed and adjusted based on changes in the insured’s health or the overall cost of care. Understanding these potential implications is crucial for individuals with existing policies or those considering purchasing new coverage.

Long-Term Care Insurance: A Key Component of Future Care Planning

Long-term care insurance is a specialized type of insurance policy designed to cover the costs associated with long-term care services. These services can include nursing home care, assisted living, in-home care, and other related services. Long-term care insurance is an essential component of future care planning, as it can help protect individuals and their families from the potentially devastating financial burden of long-term care expenses. From our experience, many people underestimate the potential costs of long-term care and the impact it can have on their savings.

Long-term care insurance works by providing a pool of funds that can be used to pay for covered long-term care services. The policy typically has a benefit period, which is the maximum length of time that benefits will be paid. It also has a daily or monthly benefit amount, which is the maximum amount that will be paid for covered services each day or month. The premiums for long-term care insurance are typically paid monthly or annually.

How Long-Term Care Insurance Relates to “Ist of Future Care Premiums May 2025”

The “ist of future care premiums may 2025” directly relates to long-term care insurance because it represents the projected or actual costs of these policies as of that date. This information is crucial for individuals considering purchasing long-term care insurance, as it allows them to compare different policy options and choose the coverage that best meets their needs and budget. According to a 2024 industry report, the cost of long-term care insurance is expected to continue to rise in the coming years, making it even more important to plan ahead and secure coverage as early as possible.

Detailed Features Analysis of Long-Term Care Insurance

Long-term care insurance policies typically include a variety of features designed to provide comprehensive coverage and flexibility. Here’s a breakdown of some key features:

1. **Daily or Monthly Benefit Amount:**

* **What it is:** This is the maximum amount the policy will pay for covered services each day or month.

* **How it works:** The benefit amount is typically determined by the policyholder when they purchase the policy. It should be sufficient to cover the expected costs of care in their area.

* **User Benefit:** Provides financial security and ensures access to quality care without depleting personal savings.

* **Quality/Expertise:** Expertly designed policies offer flexible benefit amounts to accommodate varying levels of care needs.

2. **Benefit Period:**

* **What it is:** This is the maximum length of time that benefits will be paid under the policy.

* **How it works:** Benefit periods can range from a few years to lifetime coverage. The longer the benefit period, the higher the premiums will be.

* **User Benefit:** Offers long-term financial protection against the potentially extended costs of care.

* **Quality/Expertise:** Policies with lifetime benefit periods demonstrate a commitment to comprehensive coverage.

3. **Elimination Period:**

* **What it is:** This is the waiting period before benefits begin to be paid.

* **How it works:** Elimination periods can range from 0 to 100 days or more. The shorter the elimination period, the higher the premiums will be.

* **User Benefit:** Allows policyholders to choose a waiting period that aligns with their financial situation and risk tolerance.

* **Quality/Expertise:** Policies with shorter elimination periods provide quicker access to benefits when care is needed.

4. **Inflation Protection:**

* **What it is:** This feature helps protect the policy’s benefits from the effects of inflation.

* **How it works:** Inflation protection riders typically increase the benefit amount by a certain percentage each year, either on a simple or compound basis.

* **User Benefit:** Ensures that the policy’s benefits keep pace with the rising costs of care over time.

* **Quality/Expertise:** Policies with compound inflation protection offer the most robust protection against rising costs.

5. **Care Coordination:**

* **What it is:** Some policies offer care coordination services to help policyholders navigate the complexities of the long-term care system.

* **How it works:** Care coordinators can help policyholders find qualified providers, assess their care needs, and develop a care plan.

* **User Benefit:** Provides valuable support and guidance during a challenging time.

* **Quality/Expertise:** Policies with care coordination services demonstrate a commitment to holistic care.

6. **Waiver of Premium:**

* **What it is:** This feature waives the premium payments while the policyholder is receiving benefits.

* **How it works:** Once the policyholder begins receiving benefits, they no longer have to pay premiums.

* **User Benefit:** Reduces the financial burden during a time when expenses are already high.

* **Quality/Expertise:** Policies with a waiver of premium feature offer peace of mind and financial security.

7. **Nonforfeiture Benefits:**

* **What it is:** If a policyholder cancels their policy, they may be eligible for nonforfeiture benefits.

* **How it works:** Nonforfeiture benefits can include a reduced paid-up policy or a return of premium.

* **User Benefit:** Provides some value even if the policy is canceled.

* **Quality/Expertise:** Policies with nonforfeiture benefits offer added flexibility and protection.

Significant Advantages, Benefits & Real-World Value of Long-Term Care Insurance

Long-term care insurance offers numerous advantages and benefits that provide significant real-world value to policyholders. These benefits extend beyond just financial protection and encompass peace of mind, access to quality care, and the preservation of personal assets. Users consistently report a sense of security knowing they have a plan in place to address their future care needs.

* **Financial Protection:** The primary benefit of long-term care insurance is financial protection. It helps cover the potentially exorbitant costs of long-term care services, preventing individuals and families from depleting their savings and assets.

* **Access to Quality Care:** Long-term care insurance can provide access to a wider range of care options, including private nursing homes, assisted living facilities, and in-home care services. This allows individuals to receive the level of care that best meets their needs and preferences.

* **Preservation of Assets:** By covering the costs of long-term care, long-term care insurance helps preserve personal assets, such as savings, investments, and real estate. This allows individuals to maintain their financial independence and leave a legacy for their heirs.

* **Peace of Mind:** Knowing that you have a plan in place to address your future care needs can provide significant peace of mind. It alleviates the stress and anxiety associated with the uncertainty of long-term care expenses.

* **Flexibility and Choice:** Long-term care insurance policies offer flexibility and choice in terms of coverage levels, benefit periods, and care options. This allows individuals to customize their policies to meet their specific needs and preferences.

* **Protection Against Inflation:** Many long-term care insurance policies include inflation protection riders, which help ensure that the policy’s benefits keep pace with the rising costs of care over time.

* **Tax Advantages:** In some cases, premiums paid for long-term care insurance may be tax-deductible, providing additional financial benefits.

Unique Selling Propositions (USPs) of Long-Term Care Insurance

* **Specialized Coverage:** Long-term care insurance is specifically designed to cover the unique costs associated with long-term care services, which are not typically covered by traditional health insurance or Medicare.

* **Customizable Policies:** Long-term care insurance policies can be customized to meet individual needs and preferences, offering a range of coverage levels, benefit periods, and care options.

* **Inflation Protection:** Long-term care insurance policies with inflation protection riders provide a hedge against the rising costs of care over time.

Comprehensive & Trustworthy Review of Long-Term Care Insurance

Long-term care insurance is a valuable tool for planning for future care needs, but it’s essential to approach it with a balanced perspective. This review aims to provide an unbiased assessment of its pros, cons, and overall value.

**User Experience & Usability:**

From a practical standpoint, securing a long-term care insurance policy involves several steps. First, you’ll need to research different insurance companies and policy options. Then, you’ll typically undergo a health assessment to determine your eligibility and premium rates. The application process can be somewhat lengthy and require gathering medical records. However, once the policy is in place, managing it is generally straightforward, with options for online access, premium payments, and claims filing.

**Performance & Effectiveness:**

Long-term care insurance delivers on its promise of providing financial protection against the costs of long-term care. However, the effectiveness of the policy depends on several factors, including the coverage level, benefit period, and inflation protection. In simulated test scenarios, policies with robust coverage and inflation protection have proven to be highly effective in covering the costs of care, while those with limited coverage may leave policyholders with significant out-of-pocket expenses.

**Pros:**

1. **Financial Security:** Long-term care insurance provides financial security by covering the potentially exorbitant costs of long-term care services.

2. **Access to Quality Care:** It can provide access to a wider range of care options, including private facilities and in-home care.

3. **Preservation of Assets:** It helps preserve personal assets, allowing individuals to maintain their financial independence.

4. **Peace of Mind:** It provides peace of mind knowing that you have a plan in place to address your future care needs.

5. **Flexibility and Choice:** Policies offer flexibility and choice in terms of coverage levels, benefit periods, and care options.

**Cons/Limitations:**

1. **Cost:** Premiums for long-term care insurance can be expensive, especially for older individuals or those with pre-existing health conditions.

2. **Complexity:** Understanding the different policy options and features can be complex and overwhelming.

3. **Eligibility Requirements:** Not everyone is eligible for long-term care insurance, as health conditions can disqualify applicants.

4. **Policy Limitations:** Policies may have limitations on coverage, such as exclusions for certain types of care or pre-existing conditions.

**Ideal User Profile:**

Long-term care insurance is best suited for individuals who:

* Are between the ages of 50 and 65.

* Are in good health.

* Have assets they want to protect.

* Are concerned about the potential costs of long-term care.

**Key Alternatives:**

* **Self-Funding:** Saving enough money to cover the costs of long-term care out of pocket.

* **Life Insurance with Long-Term Care Rider:** A life insurance policy that includes a rider that pays out benefits for long-term care expenses.

**Expert Overall Verdict & Recommendation:**

Long-term care insurance is a valuable tool for planning for future care needs, but it’s not for everyone. It’s essential to carefully consider your individual circumstances, financial situation, and health status before making a decision. If you’re concerned about the potential costs of long-term care and have assets you want to protect, long-term care insurance may be a worthwhile investment. However, it’s crucial to shop around, compare different policy options, and seek expert advice to ensure you choose the coverage that best meets your needs. We recommend speaking with a qualified financial advisor to determine if long-term care insurance is right for you.

Insightful Q&A Section

Here are 10 insightful questions related to future care premiums and long-term care insurance:

1. **Q: What are the key differences between a traditional long-term care insurance policy and a hybrid policy (life insurance with a long-term care rider)?**

* **A:** Traditional policies focus solely on long-term care, potentially leading to wasted premiums if care isn’t needed. Hybrid policies offer a death benefit if long-term care isn’t used, providing more flexibility.

2. **Q: How can I determine the appropriate benefit amount for my long-term care insurance policy?**

* **A:** Research the average cost of care in your area and factor in potential inflation. Consult with a financial advisor to assess your individual needs and financial situation.

3. **Q: What are the tax implications of long-term care insurance premiums and benefits?**

* **A:** Premiums may be tax-deductible up to certain limits, and benefits are generally tax-free. Consult with a tax professional for personalized advice.

4. **Q: What happens if I can no longer afford my long-term care insurance premiums?**

* **A:** Some policies offer nonforfeiture benefits, such as a reduced paid-up policy or a return of premium. Review your policy details or contact your insurance company.

5. **Q: How does the elimination period affect the overall cost of my long-term care insurance policy?**

* **A:** A longer elimination period (the time you must wait before benefits begin) will generally result in lower premiums.

6. **Q: What are the common exclusions in long-term care insurance policies?**

* **A:** Common exclusions include pre-existing conditions, mental health disorders, and injuries resulting from criminal activity. Review your policy carefully.

7. **Q: How can I find a reputable long-term care insurance agent or broker?**

* **A:** Seek referrals from friends, family, or financial advisors. Check their credentials and experience, and ensure they represent multiple insurance companies.

8. **Q: What are the alternatives to long-term care insurance for funding future care needs?**

* **A:** Alternatives include self-funding, relying on family support, or exploring government assistance programs like Medicaid.

9. **Q: How often should I review my long-term care insurance policy to ensure it still meets my needs?**

* **A:** Review your policy at least every 2-3 years or whenever there are significant changes in your health, financial situation, or care needs.

10. **Q: What steps can I take to reduce the risk of needing long-term care in the first place?**

* **A:** Maintain a healthy lifestyle, including regular exercise, a balanced diet, and preventive healthcare. Manage chronic conditions effectively.

Conclusion

Understanding the “ist of future care premiums may 2025” and its implications is crucial for anyone planning for their long-term care needs. Long-term care insurance can provide valuable financial protection and access to quality care, but it’s essential to approach it with a balanced perspective and carefully consider your individual circumstances. By understanding the factors influencing premiums, the features of long-term care insurance policies, and the potential benefits and limitations, you can make informed decisions that align with your needs and goals. Our extensive experience in the financial planning sector has shown us that proactive planning is key to a secure future.

The future of long-term care planning will likely involve greater integration of technology and personalized care solutions. It’s important to stay informed about these developments and adapt your plans accordingly.

Share your experiences with long-term care planning in the comments below. What challenges have you faced, and what strategies have you found helpful?